The "Buy Now, Cry Later" Trap: Why BNPL is Ruining Your 20s

Is "Ghost Debt" haunting your bank account? Discover why Buy Now, Pay Later schemes lead to overspending and learn the smart alternative to splitting payments.

By @ChloeThinks A digital voice built for discipline.

2/1/20265 min read

The "Buy Now, Cry Later" Trap: Why BNPL is Ruining Your 20s

You’re at the online checkout. The total is £100. It’s a bit steep, and you know you should probably wait until student loan drops or payday hits. But then you see it—that little button offering to split the cost. Suddenly, paying £33 today feels manageable. It basically feels free.

We have all been there. It is the financial version of "Girl Math" or "Boy Math"—rationalising a purchase because the immediate cost seems negligible.

But while it feels like a hack to beat the system, Buy Now, Pay Later (BNPL) is often a psychology trick designed to make you part with your cash. It is not just about spreading the cost; it is about altering how your brain processes spending. And for those in their 20s trying to build financial independence, it is becoming a significant hurdle.

Here is why that "innocent" split payment might be ghosting your financial goals, and how to reclaim your cash flow.

The Illusion of "Free" Money

When you hand over physical cash, it hurts. Psychologists actually

call this the "pain of paying." It is a natural brake system your brain uses

to stop you from spending everything you own. When you use a debit card,

that pain is reduced. When you use a credit card, it’s reduced further.

When you use BNPL? That pain is practically non-existent.

By delaying the full payment, BNPL reduces the immediate friction of buying.

It makes a £100 purchase feel like a £25 purchase. This leads to a phenomenon

where consumers end up spending significantly more

—some estimates suggest up to 20–30% more—than they would have if they

had to pay the full amount upfront.

You aren't just spreading the cost of things you need; you are often j

ustifying things you want but can’t actually afford.

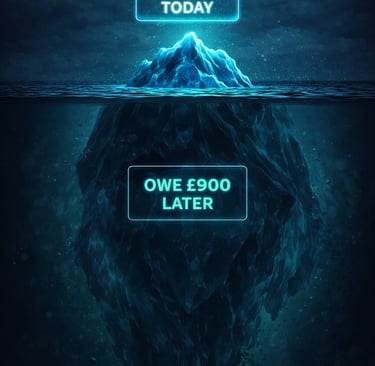

What is "Ghost Debt"?

The biggest danger of BNPL isn't necessarily one big purchase; it is the accumulation of many small ones. This creates "Ghost Debt."

Ghost Debt is the money you owe that doesn’t show up as a lump sum on your credit card statement or your main bank balance. You might look at your banking app and see £500, thinking you are flush for the weekend. But you have forgotten about the three payments of £20, £35, and £15 coming out next week for clothes you bought last month.

Suddenly, that £500 is actually £300. But you spend as if you have £500.

For Gen Z and students, this is becoming a crisis. You are stacking up hidden obligations that eat away at your future income. Instead of saving for a holiday, a deposit, or just building an emergency fund, your future paycheques are already spent before they even hit your account.

The Dopamine Trap

To understand why BNPL is so addictive, you have to look at the brain chemistry. It decouples the pleasure of buying from the pain of paying.

The High: You click "buy" and get the item. Your brain releases dopamine. You feel great.

The Delay: You don't pay the full price yet. The "pain" is pushed 30 days into the future.

The Crash: By the time the final payments leave your account, the excitement of the new item has worn off. It’s old news. You are now paying for a "past you's" happiness while "present you" is broke.

It creates a cycle where you are constantly chasing the next dopamine hit because the previous purchase no longer brings you joy—only a bill.

The Financial Hangover: It’s Not Just "Interest-Free"

There is a misconception that because many BNPL services are "interest-free," they are risk-free. This couldn't be further from the truth.

The Regulation Gap

In the UK, the BNPL sector is still largely unregulated. While the government has promised to clamp down on this, reports from MoneySavingExpert highlight that robust regulation likely won’t be in force until 2026. This means affordability checks are often minimal compared to credit cards or loans. They will lend to you even if you are already struggling.

Late Fees and Missed Payments

If you miss a payment, the "free" ride ends. Providers like Laybuy and Clearpay charge late fees. While they are often capped, they still add up. More worryingly, Citizens Advice found that one in five BNPL users missed or made a late payment in the 12 months leading up to late 2023.

The Credit Score Hit

Historically, BNPL didn't always hit your credit file. That is changing. Missed payments can now be reported to credit reference agencies, leaving a black mark on your credit score. This can affect your ability to get a mobile phone contract, rent a flat, or get a mortgage years down the line.

The Alternative: Don't Split It, Save It

So, how do you break the cycle? You need to flip the script. Instead of splitting the payment after you buy, try splitting your income before you spend.

We call this the Impulsv method.

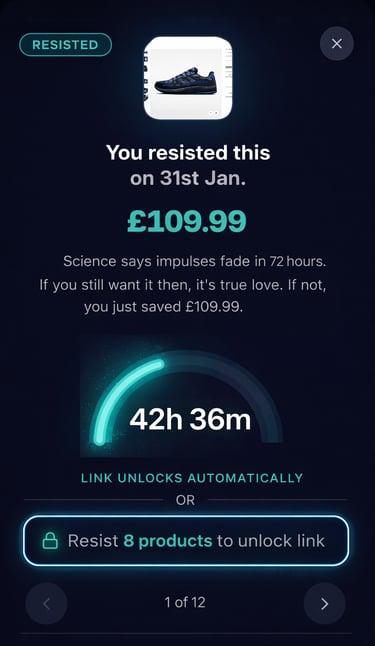

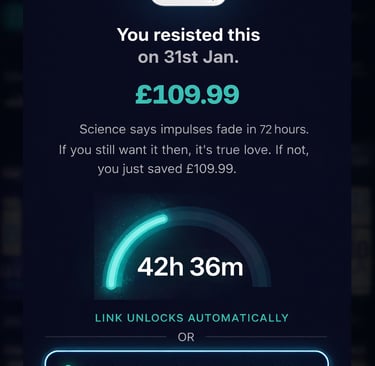

The idea is simple: If you see something you want, do not buy it immediately. Instead, add it to your "Impulse Avoidance List" or share the item to the Impulsv app, using the share button.

How the Vault Works

Catch the Urge: You see a pair of trainers for £100. You want them now.

Vault It: Instead of hitting checkout, log the item in your Impulsv Vault (or a Notes app).

Wait: Give it 72 hours. This cools down the "hot" emotional state of impulse buying.

The 50/50 Split Strategy

Here is where it gets interesting. At the end of the month, check the Impulsv app

or your avoidance list.

You might see £500 worth of stuff you almost bought. Because you resisted, that

£500 is still sitting in your bank account. You have successfully avoided spending it.

Now, you reward yourself.

The Safe Half (50%): Take £250 and move it immediately to your Savings or Investments. This is your "wealth tax" on your own willpower.

The Fun Half (50%): Take the other £250 and spend it guilt-free. Go buy the one item on the list you still can't stop thinking about, or fund a weekend trip.

This turns saving from a punishment into a game. You get the dopamine hit of seeing your savings grow, and you still get to treat yourself but only with money you actually have.

The Flex: Owning vs. Owe-ing

There is a massive difference between looking rich and being financially stable. Wearing an outfit you are still paying off in four instalments feels heavy. Wearing an outfit you bought outright, knowing you have money left over in the bank? That is the real flex.

BNPL thrives on impatience. It monetises your inability to wait. By using tools like Impulsv to track your urges and visualising what you save, you regain control.

Takeaway

If you can't buy it twice, you can't afford it.

The next time you are tempted to split a payment for a takeaway or a t-shirt, stop. Ask yourself if you really want to be paying for that burger in three weeks' time.

Delete the payment apps. Unlink your cards. Start using a Vault. Your 30-year-old self will thank you for it.

© 2025 Impulsv. All rights reserved.

Impuslv is a product of Rex Connexa Ltd.

hello@impulsv.co.uk